Global Financial Crisis

- A “Once in a Century Kind Of Event”

- The Roots of the Global Crisis: Three Complementary Perspectives

- Impact of Financial Innovations on the Size of the Global Financial System

- Impact of Growing Global Imbalances after the 1997 Asia Financial Crisis

- Impact of Central Banks’ Monetary Policies

- The Global Liquidity Boom has Fed Different Types of Bubbles

- Synchronization of Housing Price Booms Across High-Income Countries

- Contraction of the Global Financial System and Massive Wealth Losses

- Suggested Readings

- Related Documents

A “Once in a Century Kind Of Event”

Financial crises are nothing new. Over the past decade, research teams at the World Bank and the IMF had identified and studied the lessons of more than 110 financial crises of different origins, scale and duration in more than 90 countries since the late 1970s.[1] Yet, it was much more than mere self-defense when t former FRB Chairman Alan Greenspan said the present crisis has been a “once in a century kind of event,” given the complexity and magnitude of the losses and the number of countries affected. The exceptional nature of the crisis is especially visible in the United States, where the structure of the financial system has permanently changed and the redesign of a new regulatory framework has barely begun after the large-scale restructuring of the financial industry that was part of the crisis itself.

For several years, central bankers, bank regulators and economists monitoring global financial markets had worried about the widespread under-pricing of risk (Crockett 2000, BIS 2005 and 2006; IMF 2005). However, only a minority of economists and financial analysts truly anticipated the full scope of the crisis and its magnitude (See Bezemer, 2009). Everyone else was taken by surprise by this massive crisis that began with the seemingly containable U.S. subprime mortgage crisis in 2007, soon followed by the wave of financial shocks that traveled along disturbing paths throughout the global financial system.

In testimony to the U.S. Congress on 8 November 2007, FRB Chairman Bernanke initially ventured that a “ballpark estimate” of the subprime mortgage losses was $150 billion. As has happened rather consistently in major financial crises, these early estimates were not meaningful. These initial subprime losses do not compare with the projected cumulative losses of World GDP of the order of USD 4.7 trillion made a year later in November 2008, shortly after the Lehman failure of September 14, 2008. In September 2009, the sixth report of the McKinsey Global Institute (MGI) on Global Capital Markets estimated that declines in equity and real estate values wiped out $28.8 trillion of global wealth in 2008 and the first half of 2009. These losses are more than 190 times the initial U.S. subprime losses! MGI estimates of the global residential real estate losses included in these $28.8 trillion are $3.4 trillion in 2008 and nearly $2 trillion more in the first quarter of 2009. These housing losses are 36 times the initial Fed estimates of subprime losses made in October 2007. Our first financial crisis of the 21st century is indeed one of a kind in scale and global reach.

[1] See the World Bank research and policy study by Caprio and Honohan (2001). Leaven and Valencia (2008) later listed 124 crises since 1980, while Reinhardt and Rogoff (2008) identified 144 crises over the same period. Reinhart and Rogoff, in their new book on the recurrence of financial bubbles across history, This Time it is Different. Eight Centuries of Financial Folly (2009), build upon their initial experience with financial crisis while at IMF and break new statistical ground with a remarkable global database over time and across countries. The IMF World Economic Outlook of September 2009 reports on the effects of crises on the depth and lengths of losses of economic output across a large number of countries.

The Roots of the Global Crisis: Three Complementary Perspectives

Major financial and economic crises always have multiple causes. They share the same basic behavioral dimensions: risk mismanagement and risk mispricing, excessive leverage, bad lending, agency problems and euphoria.

There have been three main perspectives on the roots of the global crisis and the origins of the global liquidity boom that fed it. These are not competing views but complementary ones. Each throws light on the very long global liquidity boom that led to rapid inflation in the price of major classes of assets across the world. These three types of analyses form the basis for the corrective actions that must now be taken over a significant period of time.

The Financial Industry Perspective

The first perspective focuses on the organization, conduct and performance of the financial industry and on the governance, institutional and regulatory flaws that were revealed in the aftermath of the U.S. subprime crisis. We might thus call it the financial industry perspective. Out of a massive volume of observations, analyses and intense recommendations for action, two effective overviews of the dynamics of the global financial system were published in early 2009. The review of the crisis by Lord Adair Turner for the UK’s Financial Supervisory Authority is addressed primarily to financial authorities, regulators, policy makers and private finance executives. The Turner Review was a watershed in our early understanding of the multiple dimensions of the crisis and weaknesses in the global financial system. The Review itself is complemented by a book-length report on recommended regulatory changes to be evaluated and debated. Meanwhile, in a paper written for financial and non-financial economists, Professor Markus K. Brunnermeier (2009) of Princeton has highlighted the banking industry trends that lead up the crisis. He provides a welcome log of the core events of the crisis between early 2007 and December 2008 and points to conceptual and analytical issues that each event raises.

The International Trade and Finance Perspective

The second perspective is the international trade and finance perspective. This global crisis is not just about financial innovations, regulation and supervision errors; it also has roots in the global imbalances in international trade and capital flows that built up steadily over the past two decades and accelerated during the present decade. [2]

The extremely rapid growth of the global financial system followed the financial liberalization policies that started in the early 1980s. The balance sheet of the U.S. financial industry grew about six times faster than U.S. GDP over the entire period; its growth even accelerated during the present decade. Then another factor increasingly came into play in the late 1990s and early 2000s: global trade imbalances and the transition of the United States from a country with a small current account deficit and a balanced budget into a country with a huge current account deficit and a large budget deficit.

This deepening U.S. savings imbalance was funded by the savings coming from emerging economies of East Asia, oil exporting countries and some European states. The greater the imbalances, the more voluminous the capital flows and the greater their destabilizing potential became. In a notable speech in 2005, Ben Bernanke outlined the problems such imbalances had caused for all parties and spoke of a “savings glut” that kept global lending interest rates very low. He also pointed out that after the burst of the dot-com bubbles in 2000-2001 much of foreign savings went into U.S. Treasury and agencies securities, which in turn financed U.S. consumption and—in particular housing and other real estate assets. Thus the U.S. current account deficit financed consumption and housing. It did not go into new productive U.S. investments, which could raise productivity and contribute to long-term U.S. growth.

The Monetary Perspective

The third perspective is the monetary perspective on the principles and rules that guide the actions of central banks. What are the errors of commission and of omission by central banks that have lead them to provide excess liquidity at the wrong time of the business cycle? [3] We can expect intense debates among economists of opposing schools defending life-long professional investments in this area, because one of the factual conclusions of the crisis is that the foundations of present economic theory on which central banking policy were based are an inaccurate description of human behavior (Krugman 2009). This observation has led some analysts to conclude that present economic theory should be seen merely as “a lovely, elaborate, and fictional construction” (Rekenthaler, 2009).

[2] This perspective was especially well articulated by Martin Wolf in Fixing Global Finance (2008), an analysis that he completed shortly before the onset of our first global crisis.

[3] A representative analysis is George Cooper’s Origin of Financial Crises. Central Banks, Credit Bubbles, and the Efficient Market Fallacy (2008).

Impact of Financial Innovations on the Size of the Global Financial System

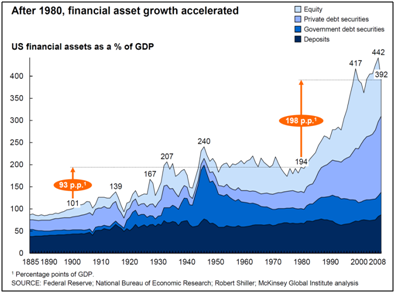

The roots of the global crisis and their scale can be illustrated with a few graphs. The 2009 annual report of the MGI on the dynamics of the global financial system extends its estimates back to 1885. The study measures the growth of four classes of financial assets: bank deposits, government debt securities and equity.

Figure 1: Accelerated Growth of the Global Financial System after 1980

Source: McKinsey Global Institute, Global Financial Markets, Entering a New Era, September 2009.

It took 100 years for the global financial system to deepen by 93 percentage points of GDP between 1885 and 1985, when the rate of growth of the financial system was closely linked to the growth of the real economy. However, it took fewer than 20 years to increase this depth by another 198 percentage points, up to a peak of 442 percent during the late derivatives bubble of 2005-2007 (Fig. 1).

The global financial system suddenly appears to be dominating the real economy and to misallocate resources to itself, including a disproportionate share of highly educated human resources compared to the other needs of the global economy. The global economy tripled from USD21.2 trillion in 1990 to USD60.7 trillion in 2008, but the global financial system quintupled from USD48 trillion in 1990to USD198 trillionin 2007 using the exchange rates of year 2008 for all previous years. Then the crisis shrunk the global financial system by USD16 trillion between 2007 and 2008. These global losses are larger than the total GDP of the United States in 2008, which was USD14.26 trillion.

Impact of Growing Global Imbalances after the 1997 Asia Financial Crisis

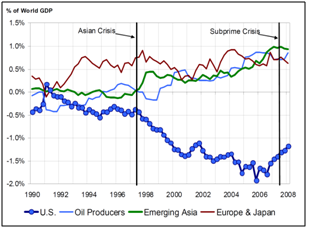

The second major contributor to the global financial crisis has been the increasing imbalances in the global economy as the U.S. current account deficit deteriorated faster after the Asia crisis, as seen in Figure 2, where the U.S. current account deficit is covered by savings from Emerging Asia, oil producing countries, Japan and part of Europe.

One important aspect of the steadily widening U.S. current account deficit from 1998 to 2006 is worrisome for the long-term growth prospects of the U.S. economy. In contrast with other cases of current account imbalances that went to finance the types of high productivity investments that raise the level of long-term growth, the U.S. deficit went to finance consumption and overinvestment in housing, the sector that contributes the least to raising productivity.

Figure 2: Deepening of Global Financial Imbalances after 1998

Source: Caballero, Farhi, Gourinchas, NBER w14521, December 2008

Impact of Central Banks’ Monetary Policies

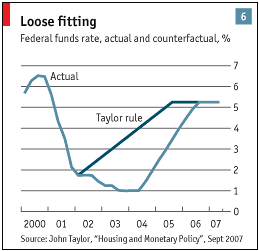

The third contributor to the global liquidity boom was the monetary policies of the U.S. Federal Reserve Board. These policies turned what could have been a self-correcting housing cycle into a massive housing bubble. This bubble burst with the U.S. subprime crisis by late 2006. The impact on the global financial system spread quickly via mortgage-related securities in early 2007 and lead to the first severe global liquidity crisis of August 2007. Figure 3, originally published by The Economist, illustrates the excessive easing of U.S. monetary policy and draws on work by John Taylor (2007), who had examined Federal Reserve policy decisions—in terms of the federal funds interest rate—from 2000 to 2006. The line that dips down to 1 percent in 2003 stays there into 2004 and then rises steadily until 2006 shows the actual interest rate decisions of the Federal Reserve. The other line, labeled the “Taylor rule,” shows what the interest rate should have been if the Fed had followed the type of policy that it had followed fairly regularly during the previous 20-year period of good economic performance. As Figure 3 illustrates, and John Taylor and other monetary economist have argued, the U.S. Federal Reserve Open Market Committee set inappropriately low Federal Funds Rates from 2002 to 2006. Adjusted for inflation, these rates were even negative in real terms in 2002 and 2003.

The excess liquidity associated with this easy monetary policy turned the U.S. housing boom that was already fed by global liquidity since around 1996 into a bubble. Given the high level of integration achieved by global financial markets, the spillover effects of U.S. monetary policies on global long-term rates and other housing markets have been significant. Very low nominal and real interest rates triggered the acceleration of global housing prices during the second phase of the housing price boom between 2002 and 2006.

A recent OECD study also finds that “within Europe the deviations from the Taylor rule vary in size because inflation and output data vary from country to country. The country with the largest deviation from the rule was Spain, and it had the biggest housing boom, measured by the change in housing investment as a share of GDP. The country with the smallest deviation was Austria; it had the smallest change in housing investment as a share of GDP” (Taylor 2008; Ahrend, Cournède and Price, 2008).

Figure 3: Easy U.S. Monetary Policy after 2002

The Global Liquidity Boom has Fed Different Types of Bubbles

Without investing further in the analysis of flaws in the structure and dynamics of the global financial system, several observations can made:

-

The much faster growth rate of the U.S. and global financial systems compared to the growth rate of GDP shows the transformation of financial markets from providers of services to the real economy into an industry that drove the real economy. Contrary to the expectation that the role of a good financial system is to allocate capital and human resources efficiently across the real economy, the evidence is that from the beginning of the decade the U.S. financial system began to invest increasingly into itself at the expense of the real economy. This predatory trend strengthened in the years immediately preceding the crisis.

-

A central feature of the massive growth of global credit has been the self-propelling nature of global liquidity due to the feedback mechanism between rising assets prices and liquidity as strong asset prices strengthen the balance-sheets of financial institutions that become more willing to lend. As a result, the risk premium embedded in interest rates becomes very low and liquidity becomes plentiful. Global liquidity and the search for nominal yields, as opposed to risk-adjusted yields, fueled five different asset and commodity bubbles (Caballero, Fahri, Gourinchas, Dec. 2008; Sornette and Woodard, 2009):

-

The ‘dot-com” or ICT bubble that began in the mid-1990s and burst in 2000-2001;

-

The transformation of the U.S. housing boom into a bubble when the U.S. Federal Reserve lowered the Fed Funds rate from 6.5 percent in 2000 to 1 percent in 2003 and 2004 in a successful attempt to limit the impact of the ICT crash as the U.S. economy went through a very mild and very short recession;

-

The financial engineering bubble built upon a variety of financial innovations such as CDOs (Collateralized Debt Obligations), CDO squared, other derivatives of debt instruments that fed the real estate boom, grew sharply after 2005 and burst with the subprime crisis itself;

-

Commodity bubbles in the prices of food, metals and energy;

-

The stock market bubble that burst in October 2007.

Synchronization of Housing Price Booms Across High-Income Countries

The combination of low interest rates and the global credit boom gave rise to housing booms across OECD countries that have been synchronized. This global housing boom was accompanied by a very significant increase in household indebtedness, as discussed further in section 3.5.2 (See Kim and Renaud, 2009).

Figure 4: Global Boom in Real House Prices, 1995–2006

Source; Kim and Renaud, 2009.

At the beginning of the present decade, the Bank of International Settlements (BIS), the OECD, and the IMF began to notice the sustained rise of housing prices in a growing number of industrial countries and the increasing synchronization of these housing price booms. The IMF in its World Economic Outlook of September 2004 documented and analyzed the co-movement of house prices across 18 industrialized countries from 1980 to 2003. France, Sweden, U.K., and the United States were found to be most strongly correlated with other countries, while Denmark, Germany and Italy exhibited the weakest correlations. Separately, Robert Shiller showed that the national U.S. house price boom since the mid-1990s was unprecedented in U.S. history, where real house prices had been flat for most of the century. U.S. housing prices were rising even faster after 2002 (Shiller 2005 and 2007). There are significant international comparability problems for housing prices. [1] Nonetheless, alternative housing price indices all show that the U.S. housing price boom was toward the lower end of these housing price booms as Figure 4 shows. Yet the U.S. housing system was at the epicenter of the global financial crisis.

The U.A.E. have been at the top of the list of countries that have experienced a massive residential construction boom from 2001 to 2007, together with Ireland, Latvia, Lithuania and Spain. In fact, Dubai’s share of the total construction sector in GDP, including residential and non-residential construction activities, was twice that of the rest of the U.A.E. (Ketels, 2009, p.18).

[1] The heterogeneity of housing price data is an impediment to reliable comparative analysis and policy making. The problem is especially conspicuous for the conduct of monetary policy across the countries of the Eurozone, where “countries have different statistics for different time periods—monthly, quarterly, half-yearly and annual—and publish them with varying time-lags. They are based on different types of data source—land registry, surveys or lenders’ valuations—and compilation methods. Data come from different parts of the house buying process—asking prices are different in nature from banks’ valuations, which in turn are different from registered selling prices. Each can be influenced at the margin by factors other than the value of the house—optimism/pessimism, business pressures and tax considerations” (Briscoe, 2008).

Contraction of the Global Financial System and Massive Wealth Losses

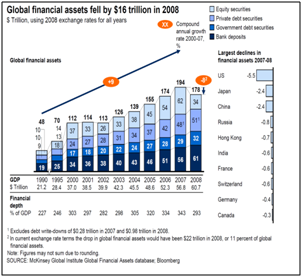

The McKinsey Global Institute’s 2009 study of the global financial system also provides estimates of losses by major countries (Figure 5). The U.S. experienced the largest wealth losses because it is the largest financial system and also the epicenter of the crisis. The U.S. losses were USD5.5 trillion for an estimated wealth loss of 38.6 percent of GDP. The magnitude of this loss ratio is very high, but there are other ways of measuring the scale of a financial crisis beyond measuring the fall in the value of financial and real estate assets.

Another perspective on the nature and impact of the crisis in the United States is to measure the change in the balance-sheet of U.S. households that had been leveraging themselves recklessly for much of the decade. Homeowners funded themselves out of the nominal capital gains on their residences by extracting wealth from the appreciating value of their houses through home equity loans (HELOC). According to one of the latest Fed estimates, U.S. households have experienced a $4 trillion loss of value since the end of 2006 on the houses they own. This loss estimate is less than the decline in households’ stock-market wealth of $10 trillion after mid-2007or the $8 trillion loss of stock-market wealth during 2000-02 (Emmons, October 2009).

Figure 5: Contraction of the Global Financial System in 2008

Source: McKinsey Global Institute, Global Financial Markets, Entering a New Era, September 2009.

A better way of measuring and comparing the true lasting burden of a crisis to society is its total fiscal cost, i.e. the increase in the stock of public debt from the year preceding the crisis. This fiscal cost is not subject to the same rapid shifts in valuation as equity prices that dominate the present MGI estimate in Figure 2. By this fiscal measure, Chile’s financial crisis of 1981—which combined the triple shock of a real estate crisis, a banking crisis and a currency crisis—has been estimated at 42 percent of GDP (World Bank, 2001, p. 83). The full fiscal cost of the current crisis to the United States remains unknown at present, but it is likely to be long-lasting. In spite of a stellar growth record after 1985 based on a profound restructuring of the Chilean economy, the remnants of the 1981 crisis were still present in the books of the central bank of Chile 15 years later, in the form of public debt.

The historical experience is that the more leveraged the growth of an economy was before a crisis, the larger the fiscal cost will be and the longer its impact. However, the record also shows that the origins of a crisis matter for the total output loss of the economy and the recovery path followed by the economy after a crisis. The four major causes of an economic crisis are: an equity bubble and crash, a real estate boom and bust, a banking bubble followed by a credit crunch, and a currency crisis (see for instance: World Bank 2001; Cerra and Saxena 2007; Claessens et al 2008; Bordo and Haubrich 2009; Cecchetti et al 2009; and the IMF’s two latest Global Financial Stability Reports of April and October 2009).

The least damaging crisis tends to be a stock market bubble. Banking crises and credit crunches are usually costly because of their direct impact on the financing of economic activities, especially when these banking crises are systemic and affect the entire banking system. Real estate and banking crises can occur independently. Real estate crises in isolation tend to be manageable. However, real estate crises and banking crises frequently occur in combination, in which case the cost of the crisis will be larger and longer-lasting. Also, there are different types of real estate crises. Several real estate crises of the 1990s in Scandinavia and Japan were dominated by commercial real estate busts rather than housing (Renaud, 1997; Mera and Renaud 2000). In contrast, the present global crisis has an important housing component, but other real sectors are often affected once again. For instance, in the United States, the crisis is beginning to migrate to commercial real estate because of the depth of the recession and the strong negative correlation between unemployment and the demand for office space.

Suggested Readings

Floods of ink have been flowing since the start of the global financial crisis. The five books listed below provide useful perspectives on the causes and consequences of the crisis for a broad audience of financial sector participants, executives and decision makers. All authors are internationally recognized leaders in their respective fields. If you can only read one book, the Rajan synthesis is recommended.

RAJAN, Raghuram [2010] Fault Lines. How hidden fractures still threaten the world economy. Princeton N.J.: Princeton University Press. 260p. Winner of the Financial Times Prize for best book of the year 2010. Probably the most balanced and best written description of the causes of the global crisis and its still evolving aftermath. The author is a former Chief Economist at IMF on leave from the University of Chicago. One of Rajan’s legitimate claims to fame is to have publicly warned about the risk of a financial crisis in a paper presented at the 2005 Jackson Hole conference of central bankers that happened to be celebrating the retirement of Fed Chairman Alan Greenspan. Rajan was harshly criticized well beyond the accepted bound of academic debates for a paper that was later widely quoted in the economic press after the crisis actually burst.

REINHART, Carmen and Kenneth ROGOFF (2009) this Time it is Different. Eight Centuries of Financial Folly. Princeton N.J.: Princeton University Press. An excellent review of past financial crises, with lessons regarding the likely aftermath of the present one. This book is a considerable extension of research work initially when both authors were at the IMF: Rogoff as Chief Economist on leave from Harvard; Carmen Reinhart as Deputy Director and Senior Policy Advisor of the Research Department.

SHENG, Andrew [2009] From Asian to Global Financial Crisis. An Asian Regulator’s View of Unfettered Finance in the 1990s and 2000s. Cambridge UK: Cambridge University Press. 487p. At a time of tectonic shifts in the structure of the global economy, Sheng’s book offers the first analysis of the Global Financial Crisis from an Asian perspective by a direct participant- observer of both the 1997 Asia Crisis and the 2008-2009 global crisis. It contains valuable chapters on the specific financial development experiences of individual Asian economies. Initially a central banker in Malaysia, Andrew Sheng has considerable operational experience across a wide range of emerging economies. He worked actively on the resolution of a number of banking crises around the world while at the World Bank. As Deputy Governor of the Hong Kong Monetary Authority, Sheng was directly in charge of the defense of the Hong Kong currency peg during the 1997 Asia Crisis. He became later Chair of the Financial Stability Forum in the years leading up to the Global Crisis. He is currently the Chief Adviser to China’s Banking Regulatory Commission.

STIGLITZ, Joseph E. [2010] Free Fall. America, Free Markets, and the Sinking of the World Economy. New York: W.W. Norton. 361 p. This book is most thoroughly documented first history of the global crisis from a US perspective. The author is a winner of the Nobel Prize in Economics in 2001 for his work on the economics of information. Stiglitz was Chairman of the Council of Economic Advisors under President Clinton and later Chief Economist at the World Bank.

WOLF, Martin [2008] Fixing Global Finance. Baltimore: Johns Hopkins University Press, 230 pp.Wolf provides the clearest explanation of how global financial imbalances were threatening the stability of the global financial systems before the crisis started. Some of these key imbalances are still with us today. The author is chief economics commentator at the Financial Times for which he writes a widely read weekly column on major economic and financial issues.

Related Documents

About the Editor

Bertrand Renaud is an international consultant and Principal of Renaud & Associates. He previously served as Advisor in the Financial Sector Development Department at the World Bank and Head of the Urban Affairs Division at the OECD.